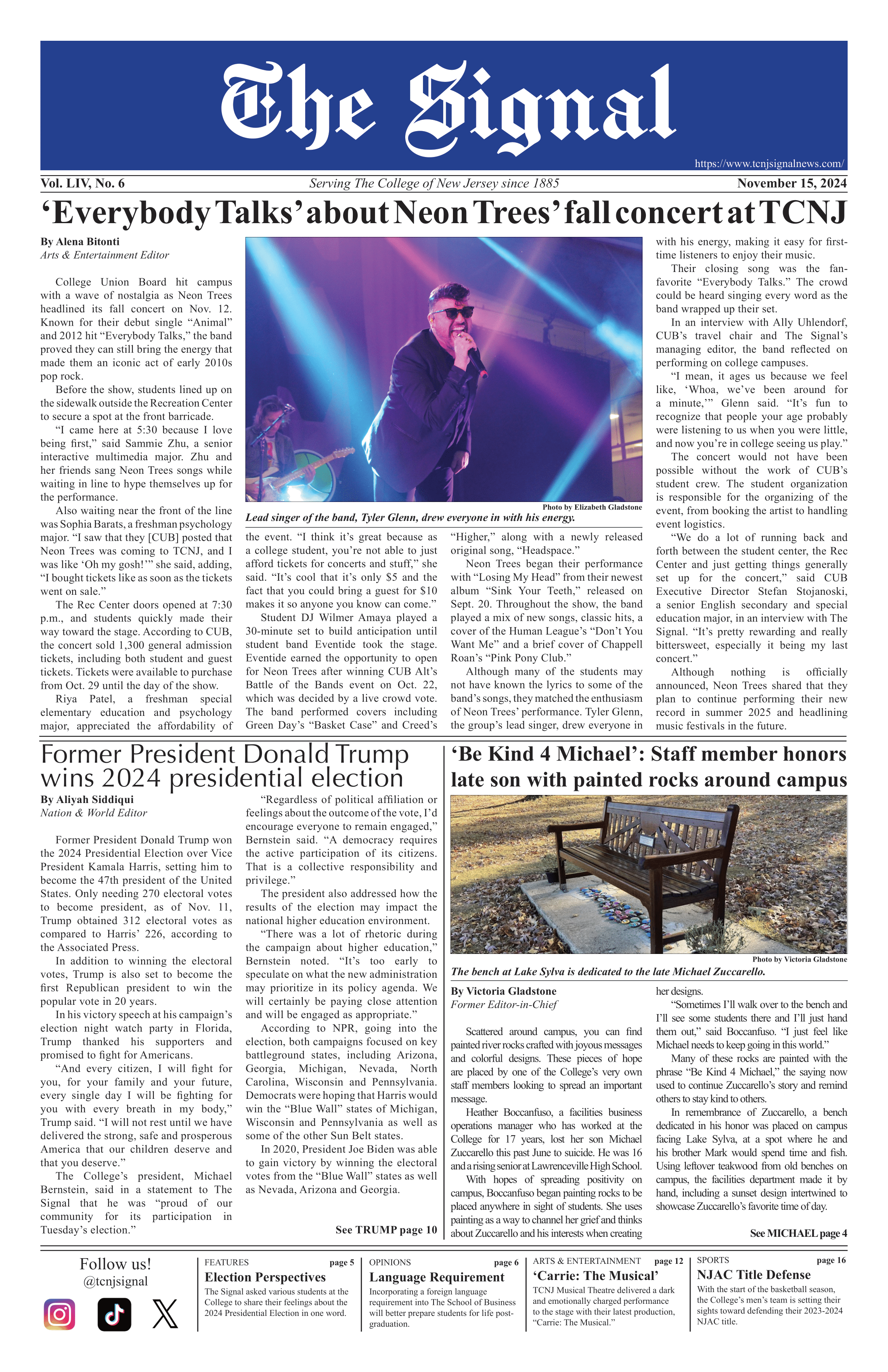

By Matthew Kaufman

Staff Writer

The Federal Reserve voted on March 16 to raise interest rates and schedule six more increases through the end of this year as a response to rapidly rising inflation, which is at the worst it has been in four decades.

As the country battled the onset of the Covid-19 pandemic in March 2020, the Federal Reserve slashed borrowing rates to next to nothing, according to the New York Times. When interest rates are low, people and businesses are encouraged to borrow more and thus spend more. Higher wages and increased consumer spending led to the rise in inflation, which forced the agency to raise rates by a quarter of a percentage point for the first time since 2018. Raising the interest rate should, in theory, reduce the amount of money being borrowed as it increases the amount that a borrower owes back.

“We’ve had price stability for a very long time, and maybe come to take it for granted – but now we see the pain,” said Jerome H. Powell, chair of the Fed, in a press conference. “We’re strongly committed, as a committee, to not allowing this higher inflation to become entrenched, and to use our tools to bring inflation back down to more normal levels.”

The move is expected to affect all aspects of borrowing, including home mortgages, car loans, credit card rates and student loans.

Zack Friedman, CEO of mentormoney.com, wrote in Forbes that most student loans, especially federal ones, are likely to have fixed interest rates, which means the interest rate on the loan is locked in at the time of borrowing and is not affected by increases by the Fed. However, some private or older federal loans carry variable interest rates, which often start out with lower interest rates but rise along with the Fed’s increases.

Student loan payments are scheduled to restart on May 1, following extensions of the pause put into place by the Biden Administration.

Those who will be applying for loans for the 2022-2023 school year will bear the brunt of the impact, according to CNBC, as the rate for federal student loans is set on July 1. Mark Kantrowitz, a student financial aid expert, told the outlet that he expects the interest rate to be between 4% and 4.5%, in contrast to the current rate of 3.7%.

Kantrowitz advises that those taking out private loans explore the options before deciding which lender to go with.

“Check several lenders’ rates by applying to multiple private student loans, then compare the cost of the various loan offers,” he said. “This will include consideration of interest rates, fees, loan discounts and other factors that affect the cost of the loan.”

Friedman recommends considering refinancing loans at a fixed interest rate. While the rate for student loan refinancing is low at a fixed rate 1.99% right now, it is expected to rise as more borrowers turn to the option following the Fed’s decision.

“If you’re pursuing student loan forgiveness or want to keep your federal benefits like income-driven repayment, then keep your federal student loans outstanding and refinance private student loans only,” Friedman wrote. “Alternatively, if you are focused on saving money and getting a lower rate or monthly payment, then you can refinance both private and federal student loans.”

But some experts are advising against refinancing immediately, according to CNBC, because the pause on interest due for student loans may be extended beyond May 1. Additionally, the Biden Administration is still exploring broader student loan cancellation, which borrowers will not be eligible for if they refinance their federal loan into a private one.

Regardless, Friedman advises that borrowers do their research ahead of May 1, when payments could be due again, and July 1, when the new rates are set.

“Make sure you evaluate all your options,” he said, “particularly with the potential for multiple interest rate increases that could make your student loans more expensive."